From Knowing What to Scope to Knowing How: Why Controlling Scoping Matters in S/4HANA Pre-Projects

Structured Controlling scoping in the S/4HANA pre-project is not a preparatory formality — it is a strategic workstream. Organizations that invest in it arrive at blueprinting with a grounded understanding of operational reality, a clear map of risks, and the evidence base for design decisions that will shape Controlling for years to come.

The problem

A global specialty chemicals producer — with manufacturing sites in Germany, the Netherlands, and Singapore — launched its S/4HANA transformation in 2022. The project was well-resourced and started on time. Blueprinting kicked off four months after project initiation.

Six months into blueprinting, the Controlling workstream ran into serious trouble.

Each production site had evolved its own cost center logic over the years. Maintenance order settlements were handled differently across sites — some costs landed on the wrong cost objects; others were reconciled manually at period-end. The costing approach for semi-finished intermediates had never been aligned with how production planning scheduled its runs. And nobody had mapped which operational processes generated Controlling-relevant data, or how that data was supposed to flow into CO.

The result: the Controlling design had to be substantially reworked. Cost object structures were redesigned. Interface specifications between plant maintenance, production, and Controlling had to be written from scratch. The delay cost the programme four months and pushed the Controlling workstream significantly over budget.

The root cause was not a shortage of skills or commitment. It was the absence of structured Controlling scoping before the transformation began — a gap that no amount of talent during blueprinting could fully compensate for.

Building on the foundation

In an earlier article, I argued that Finance and Controlling scoping in S/4HANA projects must go beyond a narrow, function-centric view — requiring three connected perspectives:

- Processes owned by Financial Accounting and Controlling,

- Functional handshakes with other business domains, and

- Value flows that translate operational events into financial insight and steering capability.

This article addresses how organizations can put this thinking into practice before the main transformation begins, through a dedicated Controlling scoping exercise in the pre-project phase.

A note on terms used throughout the article: Financial Accounting covers the external view — statutory reporting, the general ledger, asset accounting, and legal closing. Controlling covers the internal view — management accounting, cost and revenue analysis, profitability reporting, and business steering. Conflating the two in a scoping exercise tends to produce designs that serve neither well.

Why Controlling scoping matters in the pre-project

Many S/4HANA programs follow the same pattern: the Controlling workstream starts late, relies on untested assumptions, and ends up designing management accounting in isolation from operational reality. The results are gaps in blueprinting, reporting mismatches after go-live, and business cases that do not hold up under scrutiny.

Structured Controlling scoping during the pre-project addresses this directly — creating transparency, connecting the operational level with Controlling, and establishing a solid foundation before blueprinting begins.

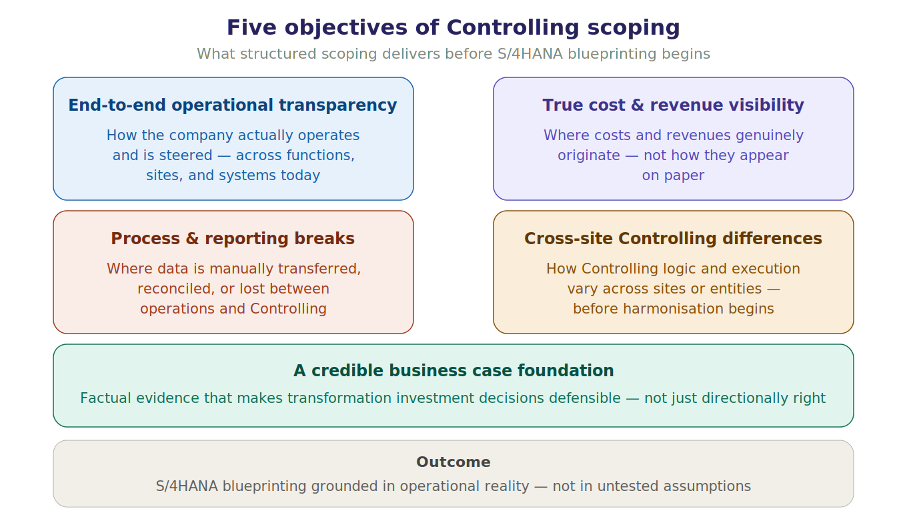

Five objectives that matter

Controlling scoping in the S/4HANA pre-project pursues five concrete goals:

- establishing a transparent end-to-end view of how the company actually operates and is steered;

- gaining a complete picture of where costs and revenues genuinely originate;

- identifying process and reporting breaks between operations and Controlling;

- comparing how Controlling logic and execution differ across sites or entities; and

- creating the basis for credible business cases for transformation decisions.

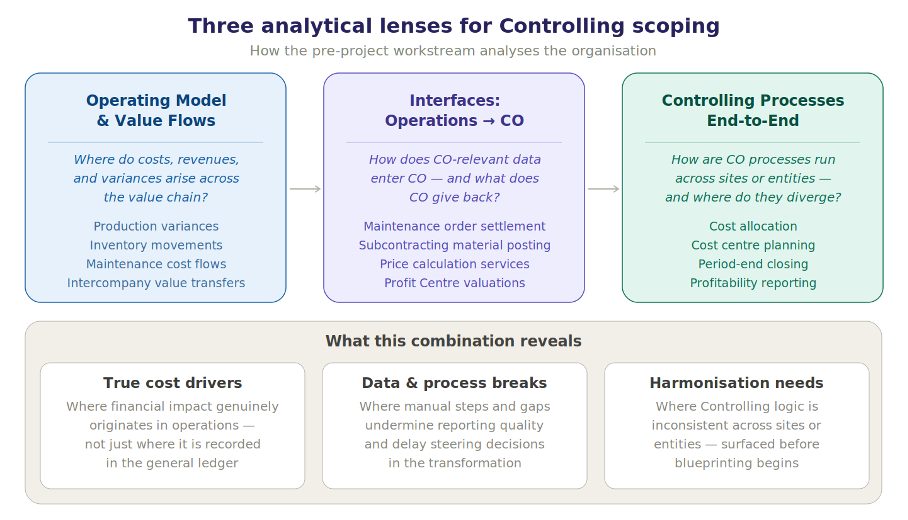

Three analytical lenses

The approach rests on three complementary ways of looking at the organization:

- Mapping the operating model and value flows;

- Mapping the interfaces between operational processes and Controlling;

- Mapping Controlling processes end-to-end.

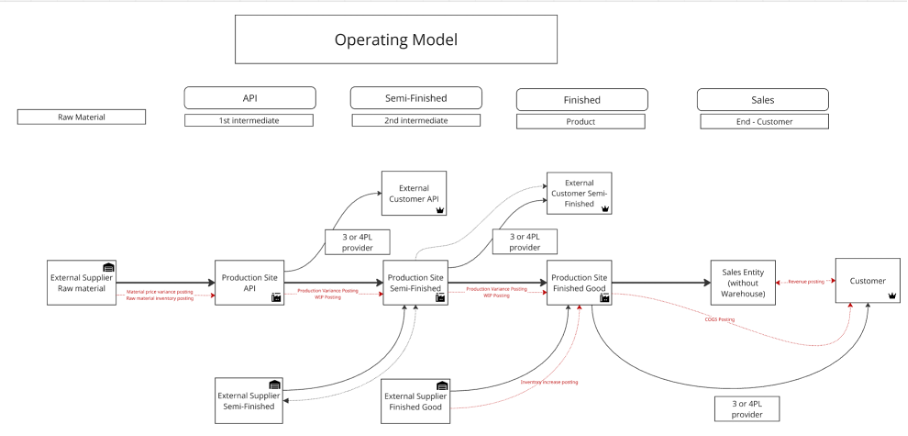

Mapping the operating model and value flows reveals where management-relevant effects actually arise: where costs are incurred, revenues generated, inventory built or consumed, and production variances captured. This prevents Controlling design from being built on abstractions rather than operational reality.

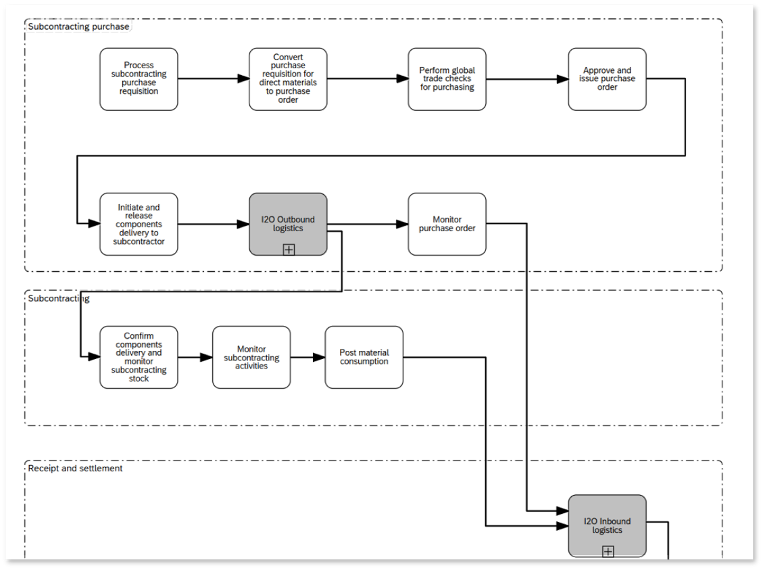

Mapping the interfaces between operational processes and Controlling focuses on where Controlling-relevant data is generated in operational processes and how it flows into CO — including the services Controlling provides back to operational areas. In a subcontracting scenario, the timely posting of material consumption as a CO process is what prevents delayed reporting and flawed steering decisions. Data breaks here directly undermine the quality of management reporting.

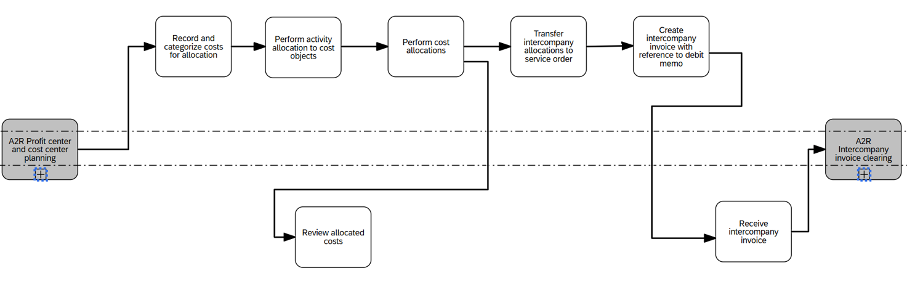

Mapping Controlling processes end-to-end identifies differences and dependencies across sites or entities, preparing the ground for harmonized steering and process execution. Cost allocation illustrates this: a complete understanding of how costs are allocated — from profit center and cost center planning, through activity allocation and cost distribution to cost objects, to the settlement of intercompany allocations — is the prerequisite for consistent profitability reporting.

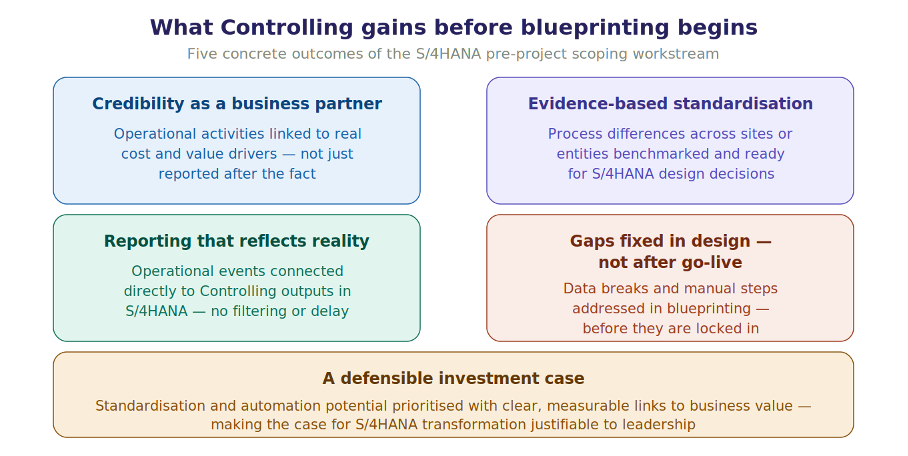

What Controlling gains from pre-project scoping

The practical benefits for the Controlling organization are significant and concrete.

Transparency over real cost and value drivers gives Controlling the credibility to engage with the business as a genuine partner. The ability to benchmark process efficiency across sites or entities enables evidence-based standardization decisions. Direct linkage between operational events and Controlling outputs means management reports reflect what actually happened — without filtering or delay. Identifying data breaks and reporting gaps before transformation means the design phase can address root causes rather than symptoms. And prioritizing standardization and automation with clear links to measurable value is precisely what makes the investment case justifiable to leadership.

Controlling scoping: a foundation for successful S/4HANA transformation

Controlling scoping in the pre-project is not a preparatory formality. It is a strategic workstream that directly determines the quality of the Controlling design in your S/4HANA transformation.

Organizations that invest in this work arrive at blueprinting with a grounded understanding of their operational reality, a clear map of risks and opportunities, and the evidence base for design decisions that will shape Controlling for years to come. Those that defer it tend to discover what they missed during blueprinting, testing, or — most expensively — after go-live.

The choice is straightforward.

At bpExperts, we support organizations in conducting structured Controlling scoping exercises as part of S/4HANA pre-project work, combining operating model mapping, interface analysis, and end-to-end process design with our Business Flows reference repository. If you would like to discuss how this approach can work for your organization, feel free to reach out.